HSA vs. FSA: What Each Account Covers and How They Differ

Both Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs) let you pay for medical expenses with pre-tax dollars. For peptide therapy that insurance refuses to cover, these accounts can reduce your effective cost by 22-37% depending on your tax bracket. But the two accounts work differently, and those differences matter for peptide therapy specifically.

HSA (Health Savings Account): Requires a High Deductible Health Plan (HDHP). Contributions roll over indefinitely. You own the account even if you change jobs. 2026 contribution limits are $4,300 (individual) and $8,550 (family). Funds can be invested and grow tax-free. You can reimburse yourself for past eligible expenses at any time, as long as the expense occurred after the HSA was opened.

FSA (Flexible Spending Account): Available through your employer regardless of plan type. Use-it-or-lose-it rule applies (with some employers offering a $640 carryover or 2.5-month grace period). 2026 contribution limit is $3,300. Cannot be invested. Must be used for expenses incurred during the plan year.

The IRS defines eligible expenses the same way for both accounts: costs of "diagnosis, cure, mitigation, treatment, or prevention of disease" that "alleviate or prevent a physical or mental disability or illness." Expenses that are "merely beneficial to general health" do not qualify.

That last sentence is the dividing line for peptide therapy. A peptide prescribed by a doctor to treat a diagnosed condition falls on the "eligible" side. The same peptide purchased for general wellness, biohacking, or optimization without a medical diagnosis falls on the "ineligible" side.

Which Peptide Expenses Qualify as HSA/FSA Eligible

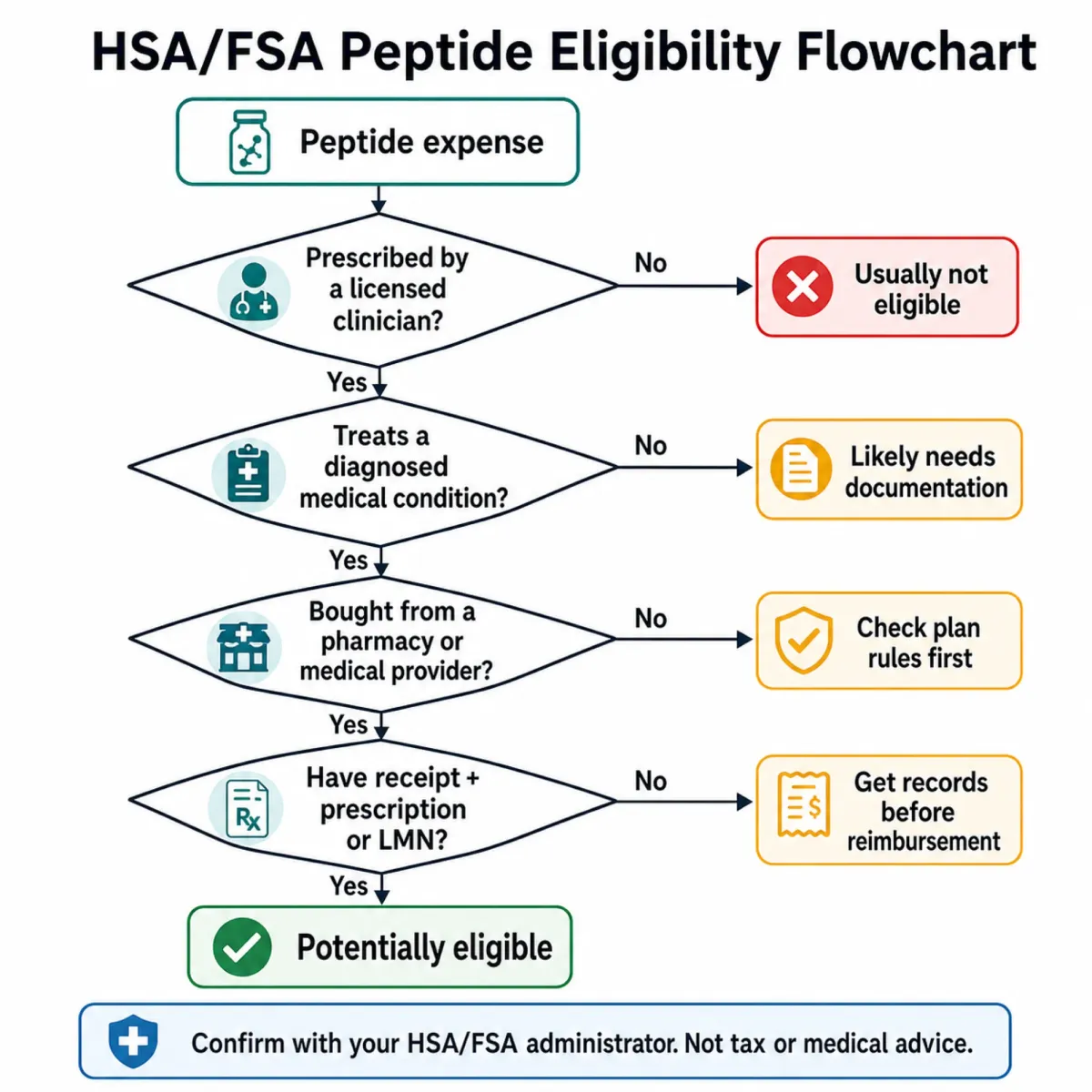

Any medicine prescribed by a health care provider is HSA- and FSA-eligible. This is the foundational rule. If a licensed prescriber writes you a prescription, and a licensed pharmacy fills it, the expense qualifies. The FDA approval status of the specific drug does not determine HSA/FSA eligibility. The prescription does.

| Peptide Category | HSA/FSA Eligible? | Key Requirement |

|---|---|---|

| FDA-approved GLP-1s (Ozempic, Wegovy, Mounjaro) | Yes | Prescription from licensed provider |

| Compounded semaglutide from 503A pharmacy | Yes (with conditions) | Valid prescription + licensed pharmacy + diagnosed condition |

| Compounded BPC-157, TB-500 from 503A pharmacy | Yes (with conditions) | Valid prescription + licensed pharmacy + diagnosed condition |

| Topical GHK-Cu prescribed for wound healing | Yes | Prescription + diagnosis (e.g., chronic wound) |

| Collagen peptide supplements (OTC) | Maybe | Requires letter of medical necessity for a specific diagnosed condition |

| Research peptides from gray-market website | No | No prescription, no licensed pharmacy, no medical documentation |

| Peptide therapy "wellness packages" without prescription | No | "Merely beneficial to general health" is explicitly excluded |

The distinction is not about the peptide. It is about the transaction. The same BPC-157 molecule is HSA-eligible when prescribed by a doctor and dispensed by a pharmacy, and ineligible when purchased from a website labeled "research use only."

The Prescription Requirement: Why It Makes or Breaks Eligibility

The IRS draws a hard line between prescribed medical treatment and self-directed wellness spending. The cost of a drug that is not prescribed by a physician is not a medical expense (with the exception of insulin and certain OTC medications for HSA/FSA purposes).

For peptide therapy, the prescription does three things:

1. Establishes medical necessity. A prescription from a licensed provider documents that a specific peptide is being used to treat a specific medical condition. This transforms the expense from "wellness" (ineligible) to "medical care" (eligible).

2. Creates an audit trail. If the IRS questions an HSA/FSA expenditure, the prescription is your primary defense. Without it, you are claiming that an unregulated substance purchased without medical oversight qualifies as medical care. That argument does not survive scrutiny.

3. Links to a diagnosis. The prescription ties the peptide to a diagnosis code (ICD-10), which is the language the IRS and your HSA/FSA administrator understand. "BPC-157 for biohacking" has no code. "BPC-157 prescribed for chronic tendinopathy (M77.9)" does.

Supplements and vitamins require a medical necessity letter from a healthcare provider to qualify. The same principle applies to peptide therapy that falls outside standard pharmaceutical channels: the provider's documentation is what makes it eligible, not the product itself.

Compounded Peptides From 503A Pharmacies: The Eligibility Case

Compounded medications are HSA/FSA eligible when they meet the same criteria as any other prescription drug: prescribed by a licensed provider, for a diagnosed medical condition, and dispensed by a licensed pharmacy.

The IRS does not distinguish between FDA-approved drugs and compounded drugs for purposes of medical expense eligibility. What matters is the prescription-pharmacy-diagnosis chain. A compounded BPC-157 formulation from a state-licensed 503A pharmacy, prescribed by a physician for a diagnosed condition like inflammatory bowel disease or chronic tendon injury, meets the IRS definition of a medical expense.

The compounding pharmacy receipt serves as your proof of purchase. The prescription serves as your proof of medical necessity. Together, they satisfy the documentation requirements for HSA/FSA reimbursement.

One practical consideration: some HSA/FSA administrators may flag compounding pharmacy charges because they do not recognize the pharmacy name or the medication. If this happens, submit the prescription and a letter of medical necessity from your prescriber. Most administrators approve the expense once documentation is provided.

Research Chemicals: Why Gray-Market Peptides Don't Qualify

Research peptides purchased from gray-market websites fail every eligibility test the IRS applies.

No prescription. Research chemicals are sold without a prescription. The vendor explicitly disclaims human use. Without a prescription, the IRS does not recognize the purchase as a medical expense.

No licensed pharmacy. Research chemical vendors are not licensed pharmacies. They do not hold state pharmacy licenses, they are not FDA-registered, and they do not operate under cGMP or 503A/503B frameworks. The IRS expects medical expenses to flow through the healthcare system, not around it.

No diagnosed condition. Without a prescriber-patient relationship, there is no diagnosis documented in a medical record. The purchase is functionally identical to buying a supplement for general health, which the IRS has explicitly excluded.

Using HSA/FSA funds for research chemical purchases is not a gray area. It is a non-qualifying distribution. If audited, you would owe income tax on the amount plus a 20% penalty (for HSA) or whatever your plan's recapture terms specify (for FSA).

Documentation That Survives an IRS Audit

The IRS rarely audits individual HSA/FSA expenses, but when it does, the burden of proof is on you. Here is the documentation stack that protects a peptide therapy claim.

| Document | What It Proves | Where to Get It |

|---|---|---|

| Prescription | Medical necessity; prescriber's clinical judgment | Your prescribing provider |

| Letter of Medical Necessity (LMN) | Specific diagnosis + why this peptide is indicated | Your prescribing provider (ask for it) |

| Pharmacy receipt / superbill | Date, amount, pharmacy name, medication name | The compounding pharmacy or telehealth clinic |

| Explanation of Benefits (EOB) or denial letter | Insurance does not cover this, justifying HSA/FSA use | Your insurer |

| Diagnosis code (ICD-10) | Specific medical condition being treated | On the prescription or LMN |

Practical tip: Ask your telehealth clinic for a superbill after every visit. A superbill is an itemized receipt that includes CPT codes (procedure codes) and ICD-10 codes (diagnosis codes). This is the format that HSA/FSA administrators and the IRS recognize. Most clinics can generate one on request even if they do not submit insurance claims.

Keep these documents for at least three years after the tax year in which the expense was incurred. The IRS statute of limitations for most audits is three years from the filing date, though it extends to six years if income is substantially underreported.

Strategies to Maximize Your Tax Benefit on Peptide Therapy

Strategy 1: Front-load HSA contributions. If you know you will pay for peptide therapy out of pocket this year, max out your HSA contribution early. Contributions reduce your taxable income dollar-for-dollar, and the funds are available immediately for qualified medical expenses.

Strategy 2: Use FSA for predictable costs. If your employer offers an FSA and you know your annual peptide therapy cost (e.g., $200/month = $2,400/year), elect that amount during open enrollment. You save your marginal tax rate on every dollar.

Strategy 3: Stack with the medical expense deduction. If your total medical expenses (including peptide therapy) exceed 7.5% of your adjusted gross income, you can deduct the excess on Schedule A. This works alongside HSA/FSA for expenses that exceed your account balance. You cannot double-dip (same expense through HSA/FSA and Schedule A), but you can use both for different expenses in the same year.

Strategy 4: Pay now, reimburse later (HSA only). HSAs have no deadline for reimbursement. You can pay for peptide therapy out of pocket today, keep the receipt, and reimburse yourself from your HSA years later. Meanwhile, the HSA funds stay invested and grow tax-free. This is the "stealth IRA" strategy that financial planners recommend for high-income earners.

Strategy 5: Get the documentation right the first time. Ask your prescriber for both a prescription and a letter of medical necessity at the same appointment. Getting these after the fact is harder and sometimes impossible if the prescriber has moved on or the clinic has closed.

Frequently Asked Questions

Can I use my HSA to buy peptides from a research chemical website?

No. Research chemical purchases lack the three requirements for HSA eligibility: a prescription from a licensed provider, dispensing by a licensed pharmacy, and documentation of a diagnosed medical condition. Using HSA funds for non-qualifying expenses triggers income tax plus a 20% penalty on the distribution amount.

Do I need a letter of medical necessity for every peptide purchase?

Not necessarily. If the peptide is prescribed by a licensed provider and dispensed by a licensed pharmacy, the prescription itself typically satisfies HSA/FSA administrators. A letter of medical necessity (LMN) is a backup for unusual expenses that might be flagged for review. Having one on file is good practice, especially for compounded medications that administrators may not recognize.

Can I deduct peptide therapy on my taxes if I don't have an HSA or FSA?

Yes, if you itemize deductions on Schedule A and your total medical expenses exceed 7.5% of your adjusted gross income. The same prescription and medical necessity requirements apply. Peptide therapy prescribed for a diagnosed condition qualifies as a medical expense under IRS Section 213(d).

Are collagen peptide supplements HSA/FSA eligible?

Only if a healthcare provider recommends them as treatment for a specific diagnosed condition and provides documentation (letter of medical necessity). Collagen supplements purchased for general wellness, skin health, or anti-aging without a medical diagnosis do not qualify. The IRS explicitly excludes expenses that are "merely beneficial to general health."

What happens if the IRS flags my HSA peptide expense?

If flagged, you will need to produce documentation showing the expense was a qualified medical expense: a prescription from a licensed provider, a pharmacy receipt with the medication name and date, and ideally a letter of medical necessity tying the treatment to a diagnosed condition. If you cannot produce this documentation, the distribution is reclassified as non-qualified: you owe income tax on the amount plus a 20% additional tax penalty. This penalty drops to 0% if you are over 65, but the income tax still applies. The statute of limitations for IRS audits is generally three years from the filing date, so retain all documentation for at least that long.

Medical Disclaimer

This article is for informational and educational purposes only and is not medical advice, diagnosis, or treatment. Always consult a licensed physician or qualified healthcare professional regarding any medical concerns. Never ignore professional medical advice or delay seeking care because of something you read on this site. If you think you have a medical emergency, call 911 immediately.